As a Non-Resident Indian(NRI) or Overseas Citizen of India(OCI), understanding and filing your Income Tax Return (ITR) is crucial to comply with Indian tax laws and avoid any potential legal issues. The ITR filing for the Assessment Year (AY) 2024-25 starts soon. NRIs who have taxable income in India need to file their ITR for FY 2023-24 by 31st July 2024. In this blog, we will walk you through the essential steps and considerations for filing ITR for NRI (AY 2024-25).

Click on the button below to file your ITR in a hassle-free way.

ITR for NRI AY 2024-25

The last date for NRIs to file their Income Tax Return (ITR) is the same as for Resident Indians. NRIs must file their Income Tax Returns (ITR) for the financial year 2023-24 (Assessment Year 2024-25) before the specified deadline of 31st July 2024.

In the further section of this blog, we will discuss the steps required for ITR for NRI along with the information related to ITR forms for NRIs.

Also Read: Income Tax e-filing: Top 10 NRI Income Tax Filing Benefits

Do NRIs need to file an ITR in India?

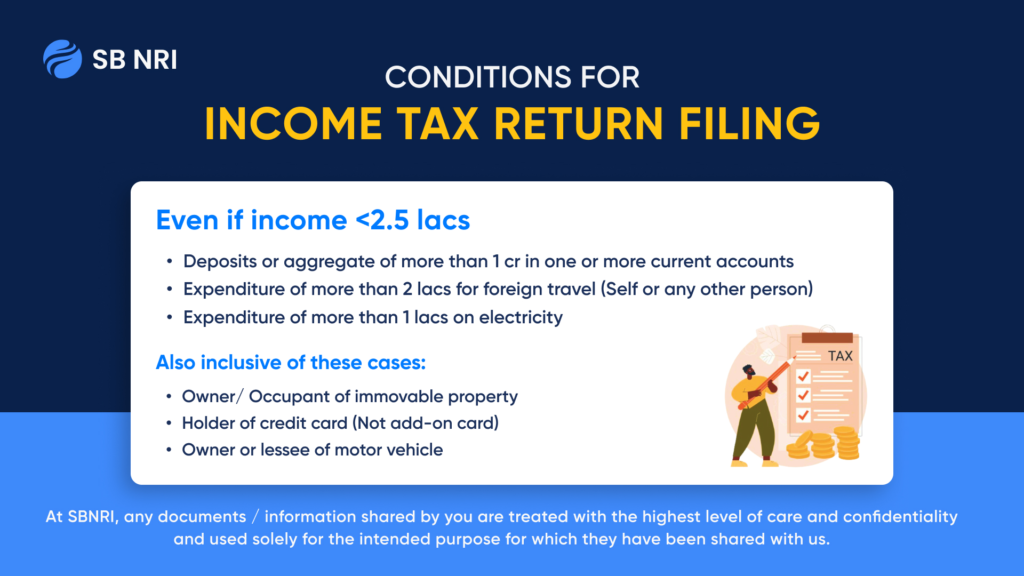

Many NRIs/OCIs do not file their income tax returns in India basis the assumption that their foreign source funds aren’t taxable in India. However, there may be transactions that they have performed in India that require them to file an NRI Income Tax Return. In many cases, NRIs/OCIs with income less than the exemption limit, i.e. Rs 2.5 lacs do not file the returns, again with the assumption that they are exempt from taxation liability.

But there are conditions where an NRI/OCI needs to file an ITR even if the income is less than Rs 2.5 lacs in India. Here are those:

- If you have deposits or aggregate of more than 1 cr in one or more current accounts

- If you spend more than 2 lacs on foreign travel

- If you spend more than 1 lacs on electricity expenditure

Furthermore, there are three additional cases where they need to file ITR for NRI in India:

- Occupant of immovable property

- Holder of credit card (Not add-on card)

- Owner or lessee of motor vehicle

Due to these discrepancies and cases where NRIs/OCIs have missed their ITR returns, Income Tax department may issue a notice or intimation to the user to verify the tax evasion and liability. It is advised that NRIs file ITR returns to abide by the compliance and avoid any notices.

Also read: Getting ITR Notice as NRI/OCI? Here’s what you need to know

Taxable Income for NRIs/OCIs

NRIs are not taxed on their foreign earnings but have to pay tax on the following income sources in India:

- Salary for services rendered in India.

- Income from residential property

- Capital gains or dividends from Indian shares.

- Any investments in India

- Income from other sources in India

Also read: Lower TDS Certificate for NRI Property Sale in India

ITR Filing for NRIs AY 2024-25: Step-by-Step Process

Here is a step-by-step guide on how NRIs can file their ITR for the Assessment Year (AY) 2024-25:

Step 1: Determining Your Residential Status

Determine your residential status and select the appropriate ITR Form based on your income sources and category.

According to the Income Tax Act, your tax liabilities are directly linked to whether you are considered a Resident, Non-Resident Indian (NRI), or Resident but Not Ordinarily Resident (RNOR). Here’s how you can determine that:

- Resident: If you spend 182 days or more in India during the financial year.

- NRI: If you spend less than 182 days in India.

- RNOR: A transitional status that applies if you have been an NRI in nine out of the ten preceding years, or have stayed in India for a total of 729 days or less in the preceding seven years.

Understanding your status is crucial as it determines your taxable income and the deductions you are eligible for. If you stayed over 182 days, you’re a resident and taxed on global income. Less than 182 days, you’re a non-resident, taxed only on Indian income. Again, taking another example, if you stay in India for 200 days in a year, you’re a resident and must pay tax on all income worldwide. If you stay for 150 days, you’re a non-resident, taxed only on income earned in India.

NRIs are required to file returns using Form ITR-2 in all cases, except for business income. For NRIs with business income, Form ITR-3 is applicable. Form ITR-1 is not available for NRIs.

Step 2: Reconciling Income and Taxes with Form 26AS

NRIs must report TDS credits and advance tax payments in Form 26AS. This will help them to avail benefits from tax treaties and also claim refunds for Tax Deducted at Source (TDS) deducted from their income. Individuals can get this Form from the e-filing tax portal.

Step 3: Calculating Your Taxable Income

NRIs are liable to pay taxes in India on various types of income such as:

- Salary for services rendered in India.

- Rental income from property.

- Interest earned on NRO (Non-Residential Ordinary) accounts.

- Capital gains or dividends from Indian shares.

- Any investments in India.

Step 4: Determining Tax Liability

Tax liability for NRIs is calculated based on the applicable NRI income tax slab rates. A basic exemption limit of Rs. 2.5 lakh applies to all NRIs before considering deductions or exemptions.

Step 5: Claiming DTAA Benefits

Under the Double Tax Avoidance Agreement (DTAA), NRIs can avoid being taxed twice on the same income. With the help of this agreement, NRIs are exempt from tax deduction in one country or taxed at a reduced rate in the home country.

Step 6: Verifying IT Returns

After filing the IT return form, it is crucial to verify the return within 30 days. NRIs can easily e-verify their IT returns from abroad using net banking, which does not require an OTP (One-Time Password).

NRI Income Tax Slab Rates for AY 2024-25 (FY 2023-24) – New Tax Regime & Old Tax Regime

| Income Tax Slab | Old Regime Slab Rates for FY 23-24 (AY 24-25) |

|---|---|

| Up to Rs. 2.50 lakh | Nil |

| Rs. 2,50,000 -Rs. 5,00,000 | 5% |

| Above Rs. 5 lakh to Rs. 6 lakh | Rs. 12,500 + 20% |

| Above Rs. 6 lakh to Rs. 7.50 lakh | Rs. 12,500 + 20% |

| Rs. 7.50,000 to Rs. 9,00,000 | Rs. 12,500 + 20% |

| Rs. 9,00,000 to Rs. 10,00,000 | Rs. 12,500 + 20% |

| Rs. 10,00,000-Rs. 12,00,000 | Rs. 1,12,500 + 30% |

| Rs. 12,00,000-Rs. 12,50,000 | Rs. 1,12,500 + 30% |

| Rs. 12,50,000-Rs. 15,00,000 | Rs. 1,12,500 + 30% |

| Above Rs. 15,00,000 | Rs. 1,12,500 + 30% |

| Income Tax Slab | New Regime Slab Rates for FY 23-24 (AY 24-25) |

|---|---|

| Up to Rs. 3 lakh | Nil |

| Rs. 3,00,000 -Rs. 6,00,000 | 5% (Rebate u/s 87A available) |

| Rs. 6,00,001 lakh to Rs. 9,00,000 | 10% (Rebate u/s 87A available for taxable income up to 7 lacs) |

| Rs. 9,00,001 to Rs. 12,00,000 | 15% |

| Rs. 12,00,001 to Rs. 15,00,000 | 20% |

| Above Rs 15,00,000 | 30% |

NRIs can choose between the existing tax regime and the new tax regime with a lower rate of taxation (Under Section 115BAC of the Income Tax Act). Given below is the table for the latest Income Tax Slabs rates for the FY 2023-24(AY 2024-25):

Note:

- Income tax exemption limit for NRI taxpayers is up to Rs. 2,50,000.

- NRIs opting for the new tax regime with lower rates will not be eligible for certain exemptions and deductions (like 80C, 80D, 80TTB, HRA).

- If they continue to pay taxes under the existing tax regime, NRIs can avail rebate and exemptions.

- NRIs can avail the new tax regime in India but they can’t claim the rebate on full tax for income up to Rs. 7 lakh. Only residents can claim the rebate on it.

Also read: TDS on Sale of Property by NRI in India [New Rates for 2024]

Who is an NRI?

An Indian national who is not considered a resident of India for tax purposes is termed a Non-Resident Indian. To determine an individual’s residential status as a Non-Resident, the provisions under Section 6 of the Income Tax Act, 1961 come into play. The criteria for being treated as a Resident in India during any previous year are as follows:

- If the individual spends 182 days or more in India during the previous year, or

- If the individual spends 60 days or more in India during the previous year and a total of 365 days or more during the four years immediately preceding the previous year.

An individual who fails to meet both of the above conditions will be considered a Non-Resident for that specific previous year.

NRI Tax Slab in India: Taxable income of NRIs

If you reside and work abroad, your tax liability as an NRI will depend on your residential status for the year. Residential status of an individual is divided into three categories – Resident and Ordinarily Resident (ROR), Resident but Not Ordinarily Resident (RNOR) and Non-Resident (NR). The scope of taxation in India based on the residential status of an Individual would be as under:

| Particulars | ROR | RNOR | NR |

|---|---|---|---|

| Income received or considered to be received in India | Taxable | Taxable | Taxable |

| Income earned or accrued in India | Taxable | Taxable | Taxable |

| Income that accrues outside India from: – Business controlled in India or profession established in India – Other income | Taxable Taxable | Taxable Nontaxable | Nontaxable Nontaxable |

Can NRIs use ITR 1 to file returns?

NRIs cannot use ITR 1. This form is exclusively for resident individuals with income from salary, one house property, and other sources, and total income should not exceed ₹50 lakh. Since they do not qualify as residents, they need to opt for other forms to file ITR for NRI.

Also read: 5 Tips for NRIs Filing Income Tax Returns in India

Types of ITR forms for NRIs for filing returns

NRIs have specific guidelines to follow when filing their income tax returns in India. There are two forms to file ITR for NRI when filing returns. The choice of the ITR form depends on the sources and amount of their income. Here’s a detailed look at the appropriate forms for NRIs:

- ITR 2: This form is suitable for filing ITR for NRI who do not have income from a business or profession in India. It covers income from salary, house property, capital gains, and other sources, making it the appropriate choice for most NRIs.

- ITR 3: NRIs having income from a business or profession in India should use this form. It accommodates a broader range of income sources, including business and professional earnings.

Also read: Types of ITR forms for NRIs

Calculate your TDS Refund with SBNRI’s TDS Refund Calculator

A TDS refund is the process of reclaiming the excess tax deducted at source by the payer if the actual tax liability of the taxpayer is lower than the TDS deducted. This situation typically arises when the income tax calculated on the total income is less than the TDS already deducted. To claim a TDS refund, taxpayers need to file an income tax return (ITR). The Income Tax Department processes the ITR and verifies the details. If the tax department finds that the TDS paid is more than the actual tax liability, the excess amount is refunded to the taxpayer.

You can easily find out how much tax refund you can get by calculating your TDS Refund from this TDS Refund Calculator.

Access SBNRI’s Exclusive NRI Taxation Guide

NRIs and OCIs can now access SBNRI’s exclusive NRI Taxation Guide covering in-depth information about DTAA, Gift Tax, Rental Income Tax, ITR Filing, Types of ITR Forms for NRIs, Capital Gain Tax, Income Tax, and more. The report will help you understand India taxation on mutual funds, other asset classes and how you can comply with the regulations.

Access NRI Taxation report here

Looking for NRI ITR Filing? Connect with SBNRI NRI Tax Expert CA Today!

At SBNRI, we have simplified ITR filing for NRIs/OCIs through a smooth digital journey. Be it Basic Filing, Advanced Filing (includes Capital Gain, etc.), or Premium Filing (Foreign Income), we can help you assess the right computation and lower your tax liability.

“We’ve helped over 500+ NRIs/OCIs file ITR returns and more than 25,000+ across other taxation services last financial year and we’d love to help you out too”

You can download SBNRI App or connect with NRI Tax Expert team directly via the button below.

FAQs

How to save on taxes in India by NRI?

NRIs can save on taxes in India by utilizing several deductions and benefits. They can claim a standard deduction of 30% and deduct property taxes and interest from a home loan.

Should NRIs file tax returns in India?

NRIs should file income tax returns in India if they earned income in India during the financial year. Their tax liability depends on their residential status.

What are 120 days rules for NRIs?

The 120 days rule for NRIs states that if they spend more than 120 days but less than 182 days in India and their total income from India is ₹15 lakh or more, they are considered “resident but not ordinary resident” (RNOR).

How to avoid TDS for NRI?

- One way is by opening a specific bank account like:

- A Non-Resident Ordinary Rupee Account (NRO)

- A Foreign Currency Non-Resident Account (FCNR)

- A Non-Resident External Account (NRE)

What is the rule for NRI in ITR?

If the annual returns for NRIs cross the basic exemption limit of Rs 2.5 lakh, NRIs should file their return. However, there are cases where the NRIs/OCIs need to file their return even if their income is less than Rs 2.5 lakh. Here are those cases:

- If you have deposits or aggregate of more than 1 cr in one or more current accounts

- If you spend more than 2 lacs on foreign travel

- If you spend more than 1 lacs on electricity expenditure

What is the penalty for not declaring NRI status?

There is no penalty for not declaring NRI status. However, we advise you to update your NRI status on the IT portal and also close your resident savings account. This will help you to avoid any discrepancies from the IT department and also help you comply with the regulations.

Do NRIs pay capital gains tax?

Yes, capital gains tax provisions for an NRI are similar to those for a resident individual except for the applicability of TDS provisions. Like resident investors, capital gains tax for an NRI depends on the holding period and the type of property sold.

How long can I maintain NRI status after returning to India?

For RNORs returning to India, they can retain their RNOR status for up to 3 years after their return. During this period, any income earned in India will be taxable, while income earned abroad will not be taxable, similar to the tax treatment for NRIs, for those 3 years post-return.

What is the 4 year rule of NRI?

An individual is considered an NRI under the Income Tax Act if they have been in India for fewer than 182 days in the preceding financial year, or if they have been in India for fewer than 60 days during the previous year and 365 days or less over the past four years.

What is the 182 days rule for NRI?

NRI can stay in India for more than 182 days during a financial year. However, doing so will change their residential status from NRI to resident. In other words, to retain NRI status, an individual must stay in India for fewer than 182 days in a financial year.

What is the 240 days rule for NRI?

The 240 days rule for NRI refers to a provision introduced in the Finance Act 2020. According to this rule, an individual will be considered an NRI if they stay in India for 240 days or less during a financial year, provided they also meet certain other conditions related to previous years’ stays in India. This amendment was made to provide more clarity and flexibility for determining NRI status, ensuring that individuals who spend a significant portion of the year outside India are not taxed as residents.

When is the last date to file an income tax return in India for NRIs?

NRIs need to file income tax returns in India before 31st July without any penalty, unless the government extends the last date.

Is NRI subject to capital gains tax on sale of a flat owned by him/her in India?

Yes. An NRI seller is liable for capital gains tax in India upon the sale of their property. The purchaser needs to deduct taxes on sale consideration. The tax deduction rate for a long-term capital gain is 20% plus applicable surcharge and cess. On a short-term capital asset, tax is deductible at 30% plus applicable surcharge and cess. However, there is a provision under the law wherein you can apply for a lower TDS certificate.

Can NRIs continue to use their resident savings account?

As per the regulations of the Foreign Exchange Management Act (FEMA), it is prohibited for non-residents to maintain resident savings accounts in India. Therefore, it is necessary to convert your resident savings account into an NRO (Non-Resident Ordinary) account. Failure to comply with this requirement and continuing to use the resident account may result in significant penalties being imposed.

How can NRIs benefit from Double Tax Avoidance Agreement (DTAA)?

NRIs have two avenues to benefit from double taxation relief, as outlined below:

- Tax Credit Method: In the Tax Credit Method, the home country allows the NRI to claim a tax credit for the tax paid in the source country where the income is earned.

- Tax Exemption Method: In the Tax Exemption Method, the income is taxed in one country and exempted from taxation in another country.

Do NRIs need to be present in India to file an ITR?

No, it is not true. NRIs can easily file and validate their income tax returns online from anywhere in the world.

Do NRIs need to pay advance tax?

If their tax liability exceeds Rs. 10,000 in a financial year, NRIs have to pay advance tax. Under Section 234B and Section 234C, interest will be applicable if you don’t pay your advance tax.

Is there any income tax for NRI in India?

An NRI’s income which is earned or accrued in India is taxable in India. The income earned outside India by an NRI is not taxable in India. Interest earned on NRE and FCNR savings and fixed deposit accounts is tax-free in India. However, interest earned on an NRO account is taxable.

What is the income tax rate for NRIs?

NRI income tax rates are mentioned in the first table in this blog along with the NRI income tax slabs.

When should an NRI file an income tax return in India?

Like resident taxpayers, an NRI must file his/her return of income in India if his/ her Indian income exceeds Rs. 2.5 lakh for the financial year. The last date for income tax filing for NRIs is 31st July of the assessment year.

Is an NRI subject to capital gains tax if he sells his house property in India?

Yes, an NRI will be liable to pay capital gains tax in India upon the sale of his flat. The buyer must deduct taxes on the quantum of gains made by an NRI. The tax deduction rate for a long-term asset would be 20%.

Can NRI claim TDS refund?

If an NRI files Income Tax Return (ITR) after the termination of the financial year in India, they can claim on the deducted TDS. NRI will need to compute his/ her income and tax liability as per the existing slab rates to claim a refund on the TDS.

Is TDS applicable to NRIs?

Interest earned on NRE and FCNR accounts is tax-free in India. Hence there is no TDS. However, interest earned on an NRO account is taxable and will be subject to a TDS of 30%. Other incomes like capital gains, fees for professional services, rental income, etc. may also be liable to TDS.

How can NRI avoid TDS?

An NRI can reduce the TDS liability on sale of his/ her property. The NRI needs to file an application in Form 13 with the Income Tax Department for issuance of certificate for lower or Nil deduction of TDS.

Can NRI claim deductions under Section 24?

NRIs can get tax deductions if they have some taxable income in India. They can claim deductions on the repayment of principal and interest components from the taxable income u/s 24, 80C and 80EE of the Income Tax Act.

Is new tax regime applicable to NRIs?

Yes new tax regime is applicable to NRIs. The new tax regime allows the basic exemption to Rs. 3,00,000. However, NRIs can’t claim the rebate on full tax for income up to Rs. 7 lakh.

What is the 80C limit for 2023-24 for NRIs?

Section 80C enables NRIs to lower their taxable income by a maximum deduction of ₹ 1.5 lakh. This deduction can be achieved by making tax-saving investments, such as paying life insurance premiums, expenses like school tuition fees. However, if NRI taxpayers choose the new tax regime, they are not permitted to claim this deduction.