Non-Resident Indians (NRI) or Overseas Citizen of India (OCI) usually have income from more than one country. Such incomes are subject to the application of tax in both countries due to local laws even though you are a tax resident in only one of these countries. In such situations, a tax residency certificate (TRC) can help NRIs/OCIs avoid paying double taxes on income earned in both their country of residence and India under the Double Taxation Avoidance Agreement (DTAA).

What is Tax Residency Certificate?

The Government of India has concluded a Double Taxation Avoidance Agreement with several countries to avoid taxing an income twice. From the year 2013, Indian citizens living in these countries can benefit from such tax treaties. A tax residency certificate (TRC) is one of the main documentary evidence to establish your tax residency and be eligible for a DTAA relief claim.

For example, an NRI earns taxable income in India and repatriates the same income to his/her country of residence after the deduction of applicable taxes, or the other way round. He/she may be liable to pay income tax in India and his/her country of residence for the same income. To avoid being taxed twice (in India and the country of your residence) under DTAA, you can obtain the TRC from the government of the country of which you are a tax resident.

Importance of TRC for Non-Resident Assessee

An NRI assessee shall obtain a TRC from the government of the country or the specified territory of which he/she is a tax resident. The TRC shall include the following details:

- Name of the NRI/ OCI assessee

- Status of the assessee (individuals, firm, etc.)

- Nationality (individuals)/ country of incorporation/ registration (firms, etc.)

- Assessee’s Tax Identification Number (TIN) in the country of residence, including a unique identification number issued by the government

- Residential status for the purpose of taxation

- Period for which the certificate is valid

- Address of the assessee for the period during which the certificate is applicable

The above details shall be provided by the NRI assessee in the Form 10F. The certificate mentioned in sub-rule (1) shall be duly validated by the Government of the country or territory of which the assessee claims to be a tax resident.

Benefits of Tax Residency Certificate (TRC)

- Double Taxation Relief: Individuals residing in India may face the burden of being taxed twice on income earned from foreign countries. For example, a resident earning income in the USA would have to pay taxes both in the USA and India. To alleviate this issue, the Government of India establishes Double Taxation Avoidance Agreements (DTAAs) with other countries. To avail the relief provided by these agreements, taxpayers must obtain a Tax Residency Certificate (TRC) to demonstrate their tax residency in India to the US tax authorities.

- Transparency in Remittance: When a resident of India exports goods or services, the foreign entity involved in the transaction often requires a TRC before remitting the payment. This requirement promotes transparency in the remittance of funds between entities located in different countries.

- Yearly Activity: Once issued, the TRC certificate remains valid until the end of the financial year. Therefore, there is no need for multiple applications or lengthy recurring processes.

Requirements for Obtaining a TRC Certificate India

To obtain a Tax Residency Certificate (TRC), the following process must be followed:

- Submit an application in Form 10F/10FA to the Jurisdictional Assessing Officer. The application should include the following information: a. Taxpayer’s status (individual, company, firm, etc.). b. Nationality or country of incorporation. c. Unique Identification Number used by the taxpayer’s resident country to identify them (e.g., Certificate of Incorporation or Aadhaar). d. Period for which the residential status mentioned in the certificate is applicable. e. Address of the assessee in the country or specified territory outside India during the relevant period.

- If the applicant is a person resident in India, the applicable form is Form 10FA. If the applicant is a non-resident, the form to be used is Form 10F.

- The Assessing Officer, upon receiving the application with all the required information mentioned above, reviews it and, if satisfied, issues a TRC in Form 10FB.

In summary, the process involves submitting the relevant application form (10F/10FA) to the Jurisdictional Assessing Officer, providing necessary details, and upon approval, receiving the TRC in Form 10FB.

How can NRIs/OCIs Obtain Tax Residency Certificate (TRC)?

The exact procedure for obtaining the TRC may be different in each country. NRI assessees can approach the competent Income Tax authority in their country of residence to obtain the TRC, for example, IRS in the USA or HMRC in the UK. To avoid any mistakes and rejections in the future, you must consult your financial advisor, the CA or CPA/ CFA, or the local bank where you have your local account. They will help you with the format to apply for TRC in the country of your residence.

Types of Income Applicable under TRC in India

While, income covered may vary depending on DTAA between India and the country where you reside, most of the following incomes are covered:

- Interest income on NRI deposits

- Dividends earned in India

- Salary earned in India

- Capital gains – short-term and long-term

- Consultancy, royalty income, etc.

- Income from the business operating in India

- Miscellaneous income

Tax Residency Certificate Format

The format of the tax residency certificate may vary from country to country.

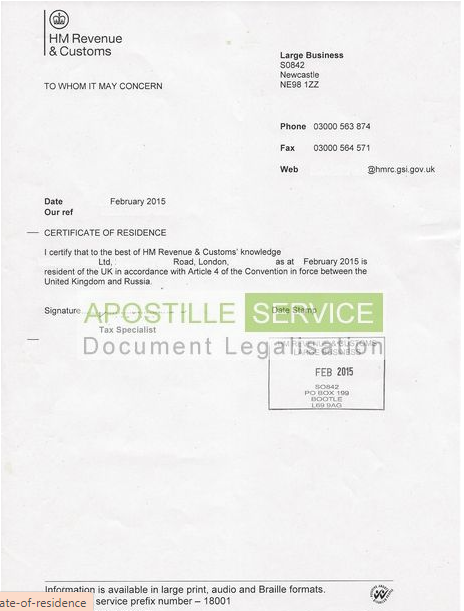

Certificate of UK Residence

Calculate your TDS Refund with SBNRI’s TDS Refund Calculator

A TDS refund is the process of reclaiming the excess tax deducted at source by the payer if the actual tax liability of the taxpayer is lower than the TDS deducted. This situation typically arises when the income tax calculated on the total income is less than the TDS already deducted. To claim a TDS refund, taxpayers need to file an income tax return (ITR). The Income Tax Department processes the ITR and verifies the details. If the tax department finds that the TDS paid is more than the actual tax liability, the excess amount is refunded to the taxpayer.

You can easily find out how much tax refund you can get by calculating your TDS Refund from this TDS Refund Calculator.

Access SBNRI’s Exclusive Guide on DTAA

NRIs and OCIs can now access SBNRI’s exclusive Guide on DTAA covering in-depth information about the applicability of DTAA, rules specific to various countries, how to avail DTAA benefits, and reduce your taxation in India and your home country.

Access NRI Guide on DTAA here

Wrapping Up

The Tax Residency Certificate (TRC) is a crucial document for Non-Resident Indians (NRIs) to navigate the complexities of international taxation. By obtaining a TRC, NRIs/OCIs can get the benefits of Double Taxation Avoidance Agreements, reduce their tax liabilities, and ensure smooth financial transactions. Understanding the importance of a TRC and the process of obtaining it is essential for NRIs to manage their cross-border tax obligations effectively.

Looking for NRI ITR Filing? Connect with SBNRI NRI Tax Expert CA Today!

At SBNRI, we have simplified ITR filing for NRIs/OCIs through a smooth digital journey. Be it Basic Filing, Advanced Filing (includes Capital Gain, etc.), or Premium Filing (Foreign Income), we can help you assess the right computation and lower your tax liability.

“We’ve helped over 500+ NRIs/OCIs file ITR returns and more than 25,000+ across other taxation services last financial year and we’d love to help you out too”

You can download SBNRI App or connect with NRI Tax Expert team directly via the button below.

FAQs

What is a Tax Residency Certificate for NRIs?

A Tax Residency Certificate (TRC) for Non-Resident Indians (NRIs) is a document that serves as proof of an individual’s tax residency status in a foreign country. It is issued by the tax authorities of the foreign country where the NRI resides or pays taxes.

Why is it necessary to obtain a Tax Residency Certificate?

A Tax Residency Certificate holds significance in order to avail relief as per the relevant Double Taxation Avoidance Agreements.

What are the details required to file Form 10FA?

The information necessary to complete Form 10FA includes:

- Assessee’s name and address.

- Assessee’s status (individual, HUF, company, etc.).

- Nationality (for individuals).

- Country of incorporation or registration (for others).

- Assessee’s email ID and PAN (Permanent Account Number).

- Duration for which the residence certificate is applicable.

- Basis for claiming resident status in India.

- Purpose of obtaining the Tax Residency Certificate.

Can an individual or an entity hold TRC from multiple countries?

Yes, an individual or entity can possess Tax Residency Certificates from multiple countries.

Is TRC mandatory for NRI?

According to the Income Tax Act of 1961, an NRI must obtain a TRC from their country of residence to claim any relief under the DTAA. Without a TRC, the relief claimed under the DTAA may be disallowed.

What is the TRC rule in Income Tax?

TRC acts as proof of residency, enabling individuals or entities to benefit from reduced or exempted tax rates as specified in the relevant treaty. Holding a TRC allows individuals or entities to access the advantages provided by tax treaties between countries.