Children’s Day is more than a mere celebration of childhood; it’s a great time to reflect on the evolving future needs of your children. For NRIs, this holds a unique importance, as balancing living abroad and planning for children’s finances can sometimes make financial planning for children’s future challenging. As children grow, the major events of their future like higher education and marriage not only brings big dreams and importance but also brings responsibilities, which needs sound financial planning. For NRIs, creating an investment plan can be a great way to meet these needs, giving children financial security while allowing them to build a foundation that will secure their future.

In this article, we’ll explore the financial steps NRIs can take to secure the future of their children. Here, we will focus on higher education and marriage, two milestones for any parents as well as children. By understanding the need of financial planning and budgeting in advance, NRIs can make sure that their children’s dreams are met with ease, no matter where life takes them.

Milestones for NRIs to Plan

1. Higher Education: For most parents, their children’s education is a high priority, and it’s becoming more expensive with time. Be it college studies or specialized courses, the tuition fees, accommodation and living expenses are rising every year. Investing can act as a powerful vehicle to build an education fund that grows with your children, thanks to compounding returns.

2. Marriage: In Indian culture, weddings hold great cultural significance and often involve high expenses. NRIs who want to celebrate their children’s marriage in India or abroad will benefit from creating a wedding fund. By starting early, NRIs can build a sizable corpus to ensure that their children have the resources for a beautiful wedding.

Why Mutual Funds Are Ideal

- Higher Growth Potential: Unlike traditional savings, mutual funds have the potential to generate higher returns over the long term. For example, equity-based mutual funds have consistently delivered good returns over long periods, beating inflation and creating wealth.

- Professional Management: Mutual funds are managed by professional fund managers, meaning your investments are handled by experts who make sure to maximize returns and reduce risk.

- Flexible Options: With a range of mutual funds available—equity, debt, hybrid, or sectoral, NRI investors can choose a mix that matches their risk capacity and timeline, helping them grow wealth effectively for their children’s future.

How Mutual Funds Can Secure Your Child’s Financial Future

- Systematic Investment Plans (SIPs): SIPs offer a disciplined and consistent approach to investing, helping NRI parents create a financial base over time. Through SIPs, you can start small and invest monthly, build your portfolio and manage your funds over time. Regular investment in mutual funds will grow over time with compounding.

- Lump-sum Investment: Mutual funds provide a lot of options to invest in based on individual goals and priorities. For your child’s education fund, you can consider investing lump-sum in balanced funds if you’re looking for moderate growth with lower volatility. This will provide stability, ensuring you won’t face significant fluctuations when you will need those funds. For wedding expenses, investing a part of your savings in equity mutual funds or hybrid funds today is ideal if you are planning to invest for 10-20 years. Since marriage usually happens 5-10 years after higher education, equity funds will get more time to grow your wealth.

Steps to Start Investing in Mutual Funds

- Define Your Goals: Start by setting specific goals for your children’s education and marriage. Estimating the cost of these expenses and time horizon for each goal will help you select suitable funds and determine the amount you need to invest today (or regularly in case of SIP).

- Choose the Right Funds: Not all funds are equal, and selecting the right ones is crucial. If education is 10 to 15 years away, prioritize equity mutual funds. For shorter-term goals like expenses in 5 years, consider balanced or debt mutual funds to safeguard against short-term market fluctuations.

- Choose Between Lump Sum and SIP: If you want to invest larger amounts periodically, lump sum investments work well, especially when markets are correcting and provide great opportunities to invest. And if you want to invest a small amount of money regularly, say monthly, you can go for SIPs.

- Monitor and Review Regularly: Financial goals and market conditions can evolve over time. A yearly review of your portfolio will help you track your expected expenses and portfolio, which is important to stay on track to reach your financial goals.

Advantages of Investing in India

Investing in India offers unique benefits to NRIs, which include:

- High Growth Potential: Indian markets have historically shown strong growth, the reason being a growing economy and expanding industries. Investments in India can yield great returns, helping NRIs build wealth faster compared to developed economies with slow growth.

- Currency Diversification: For NRIs, having assets in different currencies is beneficial. By investing in India, NRIs can hold wealth in Indian Rupees, providing a diversification against currency-specific fluctuations.

- Family Legacy: For NRIs with roots in India, investing in the country is more than profits. It builds a legacy that connects their children to their heritage.

Growth Potential with Mutual Funds

If you invest in mutual funds, the upside potential is significant. Let’s take an example: If you invest INR 10 Lakhs today in an equity mutual fund with an average annual return of 12%, over 15 years, you could build a corpus of XYZ, which can be a significant amount to meet expenses such as higher education or wedding of children. Starting early and staying invested over the years can multiply your wealth effortlessly.

Let’s understand the power of regular investing and compounding:

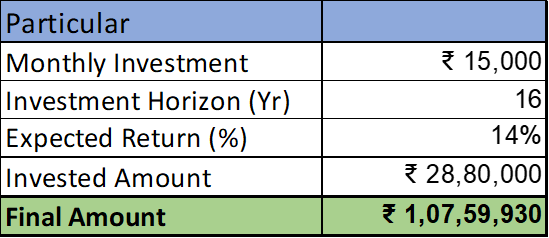

Say your child is 5 years old right now and would pursue higher education after 16 years (i.e. at the age of 21). With a monthly investment of Rs. 15,000 at a 14% annual return, you will have Rs. 1 Cr+ for your kids’ education in 16 years.

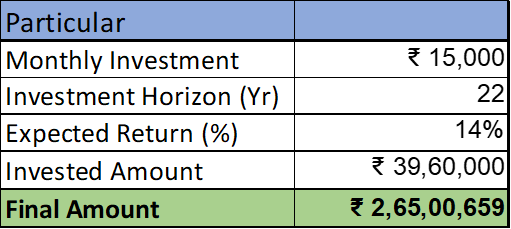

Now if you start another SIP of the same amount of Rs. 15,000/month and keep investing for 22 years for your child’s marriage (i.e. until your child turns 27), your portfolio would be worth Rs. 2.65 Cr.

This clearly represents how compounding can do wonders for your children’s financial future, and how starting from a monthly SIP of Rs. 15,000 can help you secure your children’s financial future to meet the biggest milestones of their life.

Conclusion

By taking the first step on this Children’s Day, you are not only securing your children’s future but also giving them the gift of financial security to their dreams without financial worries. For NRIs, planning these investments early helps them build wealth over time to bear rising education and wedding costs. Remember that this gift goes beyond finances, providing peace of mind, stability, and security. So start small, stay consistent, and secure your children’s future.

If you need a helping hand to help you navigate the complexity of financial planning and investments, connect with us and we will guide you throughout the process.

SBNRI is an authorized Mutual Fund Distributor platform & registered with the Association of Mutual Funds in India (AMFI). ARN No. 246671. NRIs willing to invest in mutual funds in India can download the SBNRI App to choose from 2,000+ mutual fund schemes or can connect with the SBNRI wealth team to better understand Mutual Fund investments.

Disclaimer: This blog has been written exclusively for educational purposes. The securities mentioned are only examples and not recommendations. It is based on several secondary sources on the internet and is subject to changes. Please consult an expert before making related decisions. SBNRI does not intend to predict future returns, please read all related documents before investing.

Frequently Asked Questions

Why should one invest early for their children’s future?

Investing early allows NRIs to enjoy the power of compounding, which helps them meet long-term goals like higher education and marriage of children.

How often should an individual review and adjust their investments?

An annual review works well to ensure that the investments align with evolving goals of investors and market conditions. Investors can go for a half-yearly review as well to stay better aligned with their goals.

What is the best way for NRIs to start investing in mutual funds?

NRIs can open an NRE or NRO account to invest in India, depending on their individual needs. Consulting with a financial advisor to navigate through the process effortlessly.